There is a story Washington tells itself about sovereign debt.

The story goes like this: the numbers are large, the trajectory is concerning, but the United States has always found a way. Foreign buyers absorb the supply. Institutional demand holds. The dollar remains the world’s reserve currency because there is no credible alternative. Adjustments will be made eventually. The system is self-correcting.

That story is financially convenient. But structurally, it is becoming incomplete.

The national debt has breached $39 trillion. The move from $38 trillion to $39 trillion took less than five months, a pace of accumulation historically associated with total-war mobilization rather than peacetime governance. The annual net interest burden is approaching $1 trillion, a figure that now rivals the entire discretionary allocation of major federal departments.

Foreign central banks are quietly rotating out of Treasury allocations. Institutional buyers face duration risk and regulatory constraints that limit how much new supply they can absorb. Recent auction data has signaled weaker demand and rising tail risk across multiple issuance windows.

In that environment, a new mechanism is emerging. It does not arrive through emergency legislation or a dramatic policy announcement. It arrives through market infrastructure, deliberate legislative architecture, and the quiet logic of reserve engineering. It is called the digital dollar. And understanding what it is actually doing requires looking past the headline and into the plumbing.

The $39 Trillion Fiscal Context

The fiscal position of the United States has reached what analysts describe as a structural inflection point.

The Congressional Budget Office projects that net interest payments on the federal debt will exceed $1 trillion annually, consuming a growing share of both mandatory and discretionary budget capacity. When interest payments begin to crowd out public investment and federal transfers, the government faces a compounding problem.

Borrowing to service existing debt accelerates new debt accumulation. That acceleration then requires either deeper cuts, higher taxes, broader monetization, or the identification of new demand pools capable of absorbing ongoing issuance at scale.

What is most significant about the current moment is not the nominal size of the debt itself. Sovereign debt of this scale has existed before in different historical contexts. What is significant is the velocity of accumulation alongside the simultaneous erosion of the traditional buyer cohorts that have historically made that debt manageable.

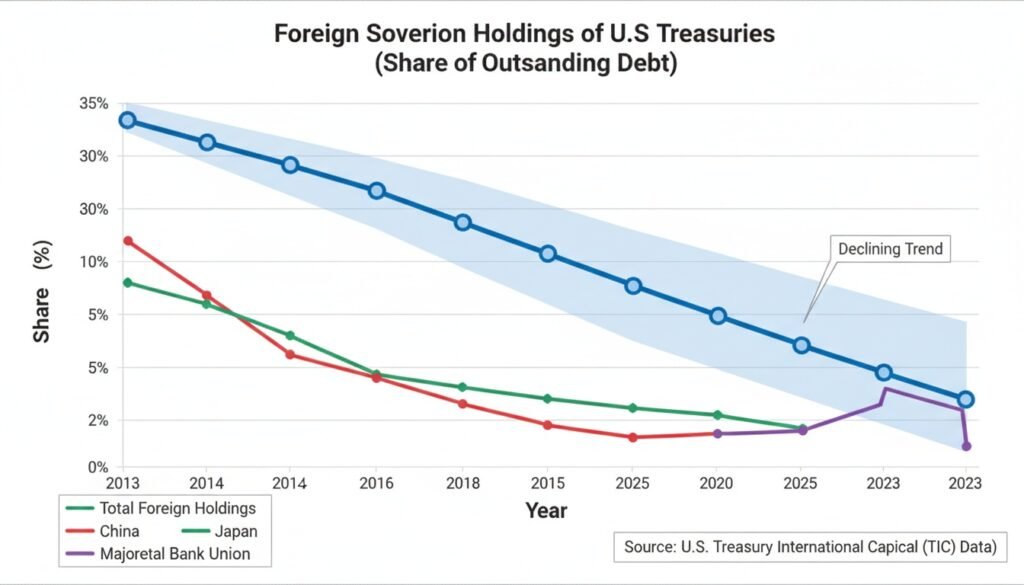

Foreign sovereign holdings of U.S. Treasuries have declined as a share of outstanding debt over the past decade. Data from the U.S. Treasury’s Treasury International Capital system documents a gradual but sustained rotation away from U.S. government securities among several major central bank holders.

The reasons include geopolitical realignment, active de-dollarization programs, and the diversification of foreign exchange reserves toward gold and bilateral currency arrangements. This is not a crisis-level collapse in foreign demand. It is a structural drift with long-term implications for how the United States finances its obligations.

At the institutional level, commercial banks and pension funds are navigating the tension between duration risk and regulatory capital requirements. The volume of new Treasury supply entering the market each quarter creates absorption challenges for buyer cohorts already carrying significant fixed-income exposure. That constraint does not disappear simply because supply keeps growing.

The question, then, is where the next wave of demand originates. The answer being assembled in Washington is not a single solution. It is a new architecture. And its central feature is the digital dollar.

The Stablecoin Mechanism

The emergence of dollar-denominated stablecoins represents a structural answer to that question, though it is not the only one, and it is not a complete fiscal cure.

Stablecoins like USDT and USDC are not primarily speculative instruments. They function as digital proxies for the U.S. dollar, operating on blockchain rails that allow peer-to-peer transfer of dollar-equivalent value without requiring the sender or receiver to hold a traditional bank account. Their relevance to sovereign debt financing is embedded in the reserve model that makes them work.

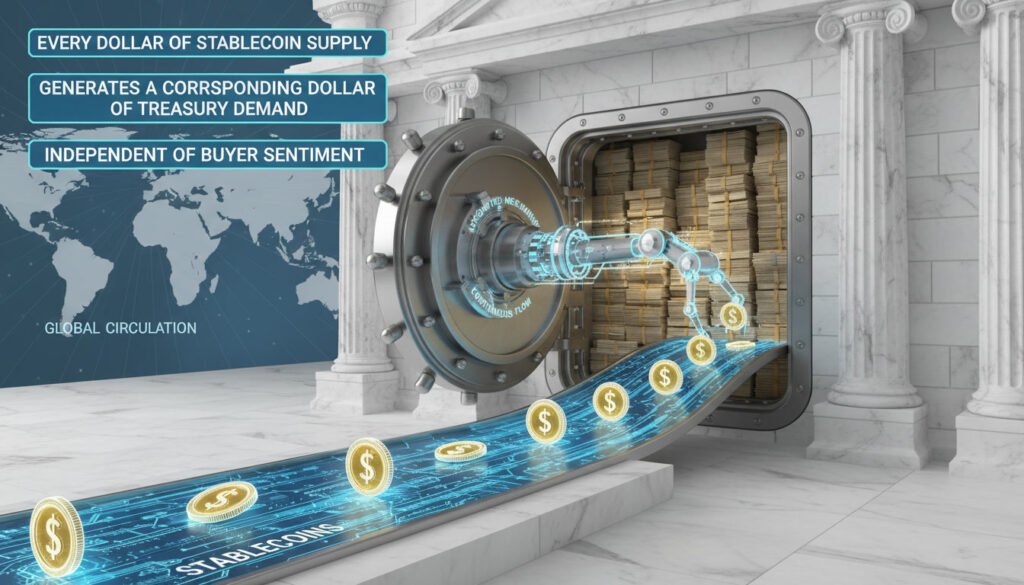

To maintain a 1:1 peg with the dollar, stablecoin issuers must hold equivalent reserves in high-quality liquid assets. The dominant reserve choice, by both regulatory preference and liquidity logic, is short-duration U.S. Treasury securities. Every dollar of stablecoin supply that enters global circulation therefore generates a corresponding dollar of Treasury demand. The mechanism is automated, continuous, and operates independent of institutional buyer sentiment at any given auction window.

This is the core structural logic that has drawn the attention of both Treasury officials and monetary economists. When a vendor in Lagos accepts USDC for a transaction, or a family in Buenos Aires holds USDT to protect savings against peso devaluation, that demand flows directly into the U.S. sovereign balance sheet through the issuer’s reserve requirement. The end user is not consciously lending to the U.S. government. But structurally, that is precisely what is occurring.

The scale of this mechanism remains modest relative to total sovereign issuance. But the growth trajectory of stablecoin market capitalization, combined with the legislative architecture now being built around it, indicates that this is not a peripheral phenomenon. It is an emerging structural pillar of the dollar’s transmission infrastructure.

Every new holder of a regulated stablecoin becomes, in structural terms, an automated and non-institutional lender to the U.S. government. That process does not require a Treasury auction. It does not require a broker, a central bank allocation, or a custodian. It requires only a mobile phone and a digital wallet.

Legislative Architecture: The GENIUS Act

Washington’s posture toward stablecoins has shifted from cautious skepticism toward deliberate strategic integration.

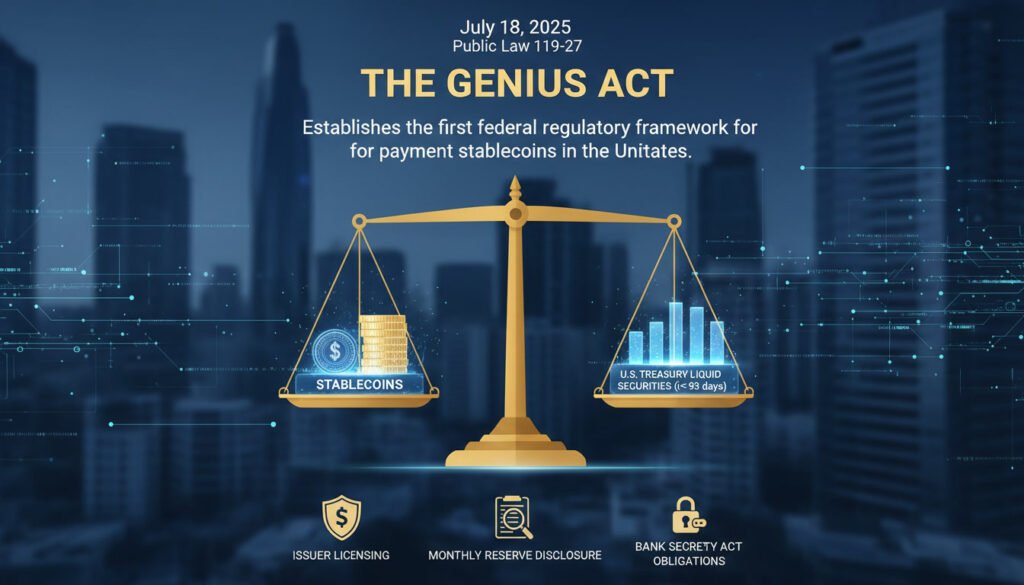

The GENIUS Act, signed into law on July 18, 2025, as Public Law 119-27, establishes the first federal regulatory framework for payment stablecoins in the United States. Its core requirement is that permitted issuers maintain reserves backing outstanding stablecoins on at least a 1:1 basis, with those reserves consisting of specified high-quality liquid assets.

Short-term U.S. Treasury securities with a remaining maturity of 93 days or less occupy a central position in the statute’s list of permitted reserve categories. The Act also imposes Bank Secrecy Act obligations, issuer licensing requirements, and monthly reserve disclosure standards.

Taken together, these provisions do not merely regulate a crypto-adjacent market. They formalize stablecoins as a regulated instrument of the dollar’s global circulation and, by extension, as a legally defined conduit for sovereign debt demand.

That distinction matters for the question of scale. When stablecoins exist in legal ambiguity, institutional participants cannot scale their involvement with confidence. Capital follows clarity. By removing the regulatory tail risk for banks, payment processors, and technology companies seeking to operate in the digital dollar space, the GENIUS Act functions as a formal on-ramp for institutional participation in a previously fragmented market.

The White House fact sheet accompanying the signing stated explicitly that the Act “will generate increased demand for U.S. debt and cement the dollar’s status as the global reserve currency by requiring stablecoin issuers to back their assets with Treasuries and U.S. dollars.” The government’s own framing of the legislation confirms that the sovereign debt absorption function is not an incidental byproduct of consumer protection regulation. It is a stated strategic objective.

Additional market structure legislation, including the CLARITY Act, extends the architecture further into the broader financial system by addressing the integration of digital assets into private sector and institutional banking infrastructure. Where the GENIUS Act establishes the foundational rules for payment stablecoins, the CLARITY Act aims to expand the range of participants who can operate within those rules without creating systemic ambiguity.

Together, these legislative instruments represent the deliberate codification of stablecoins as tools of financial statecraft. The U.S. government is not simply tolerating the digital dollar ecosystem. It is building the rails for it.

The Unbanked Population and the Expansion of Dollar Reach

The strategic logic of the digital dollar extends beyond domestic debt management.

The World Bank’s Global Findex Database 2021 estimates that approximately 1.4 billion adults globally remain unbanked, meaning they lack access to a formal financial account. This population is not uniformly distributed. It is concentrated in sub-Saharan Africa, South Asia, and parts of Latin America, regions that also exhibit the highest rates of local currency volatility and the weakest institutional protections for private savings.

This population is not, however, without mobile technology. According to the Global Findex data, approximately 1.1 billion of those 1.4 billion unbanked adults, roughly two-thirds, already own a mobile phone. The infrastructure for digital transactions exists where the banking infrastructure does not.

Stablecoins operate on that existing infrastructure. A mobile wallet holding USDC is, in functional terms, a dollar-denominated savings instrument that requires no branch network, no credit history, and no correspondent banking relationship. For an individual in a country experiencing sustained monetary inflation, the accessibility of a digital dollar represents a qualitatively different kind of protection than local financial institutions can offer.

The strategic implication for the United States is consequential. The traditional addressable market for dollar-denominated financial products has historically been bounded by the reach of the formal banking system. That boundary is dissolving. As digital dollars extend into populations that were previously outside the dollar’s practical reach, the base of global demand for dollar-denominated instruments expands correspondingly.

Each new user of a regulated stablecoin is, structurally, a new participant in the Treasury demand mechanism. The cumulative effect of that expansion across hundreds of millions of previously unbanked individuals represents a meaningful directional shift in the sovereign debt absorption equation. It does not solve the $39 trillion problem immediately. But it changes the composition of the global creditor base in ways that do not depend on the policy decisions of any single foreign central bank.

Foreign Monetary Sovereignty and the Geopolitical Friction

The expansion of digital dollar reach does not occur in a geopolitically neutral environment.

For foreign monetary authorities, the widespread adoption of dollar-denominated stablecoins by their domestic populations represents a form of monetary competition that operates below the threshold of formal dollarization. When citizens of a country choose to hold USDT for savings, transact in USDC for commerce, or exit local currency positions via a mobile wallet, they are exercising a form of monetary exit that does not require any formal policy change by their government.

The structural effect is what economists describe as currency substitution. When a meaningful share of domestic monetary circulation shifts toward a foreign-denominated instrument, the domestic central bank loses effective control over a corresponding portion of the money supply. Its capacity to conduct monetary policy, manage inflation, and maintain the institutional relevance of local financial intermediaries is diminished proportionately.

This creates a predictable political dynamic. Foreign governments that perceive this process as a threat to monetary sovereignty will respond with regulatory restriction. Several emerging market jurisdictions have already enacted or proposed limitations on stablecoin adoption. Those restrictions should be read as a signal rather than a verdict.

When a government moves to ban or severely limit digital dollars within its borders, it is not demonstrating the inefficacy of the U.S. strategy. It is acknowledging that the competitive appeal of dollar-denominated digital instruments is sufficient to displace local alternatives at scale. Resistance is a form of confirmation. The friction generated by the digital dollar’s expansion is proportional to how effectively it is working.

That dynamic is not a side effect to be managed. It is a strategic indicator to be monitored.

Monitoring the Transition: Signals for Structural Analysis

The digital dollar transition is not a binary event. It is a gradual structural shift that will manifest through observable signals across multiple domains.

The first domain is legislative implementation. The GENIUS Act establishes the framework, but the operational details will be determined by regulatory rulemaking. The specific definitions of permitted reserve assets, the capital requirements for issuers, and the scope of bank participation will shape how quickly stablecoin issuers can scale their Treasury demand. Narrow or restrictive reserve definitions would limit absorption capacity. Broad and inclusive definitions would accelerate it.

The second domain is stablecoin market capitalization. The total regulated stablecoin market cap functions as a real-time proxy for global dollar demand outside the traditional banking system. Growth in that figure, particularly in jurisdictions with weak local currencies, indicates the expansion of the Treasury demand mechanism into new pools of global liquidity.

The third domain is foreign regulatory response. The frequency and severity of foreign government actions to restrict stablecoin adoption provide a lagging indicator of digital dollar penetration. A map of active stablecoin restrictions is, in structural terms, a map of where the dollar is successfully competing with local monetary alternatives. Heightened resistance in emerging markets is not a sign of failure. It is a confirmation of traction.

The fourth domain is Treasury auction composition data. If the digital dollar mechanism is functioning as a structural demand supplement, its effects should become visible in auction tail statistics, bid-to-cover ratios at the short end of the yield curve, and shifts in indirect bidder participation relative to primary dealer takedown. Improvement in those metrics, occurring concurrently with stablecoin market growth, would constitute measurable evidence of the transmission mechanism operating at scale.

No single signal is conclusive. The pattern of signals taken together is what warrants sustained analytical attention.

The Structural Pattern

The $39 trillion debt figure will continue to appear in headlines as a symbol of fiscal dysfunction. That framing is not inaccurate. But it is incomplete.

What those headlines rarely examine is the infrastructure being deliberately constructed around the problem. The GENIUS Act, the forthcoming CLARITY Act, the systematic expansion of stablecoin reach into unbanked populations, and the architectural decision to embed Treasury securities into the statutory reserve requirements of the digital dollar system are not accidental policy choices. They reflect a strategic recognition that the traditional demand architecture for U.S. sovereign debt is under structural pressure and that a new architecture must be built before the old one fully erodes.

That new architecture does not announce itself as a response to the debt crisis. It presents itself as financial innovation, consumer protection, and digital inclusion. But its structural function is to extend the dollar’s monetary reach, automate non-institutional demand for Treasury securities, and create a new global base of sovereign creditors who carry the dollar in their pockets rather than on their central bank balance sheets.

The pattern is not without precedent. Dominant monetary powers have always sought to distribute the costs of their sovereign issuance across the broadest possible creditor base. What is new is the mechanism. And the mechanism, this time, runs on a mobile phone.

Tier 5 Synthesis

Built from the tiers below: This is the author’s synthesis of the documented pattern, not a standalone evidentiary claim.

If we step back from the individual policy instruments and look at the direction of travel, a deeper logic comes into view. The digital dollar is not simply a technological upgrade to payment infrastructure. It is the latest iteration of a recurring pattern in which dominant monetary powers solve fiscal stress not by reducing the debt but by expanding the pool of creditors available to absorb it.

What is structurally significant about this moment is the method. Every previous expansion of the dollar’s creditor base required institutional intermediaries. Foreign central banks, commercial banks, pension funds, and primary dealers served as the gatekeepers through which sovereign debt demand was aggregated and transmitted. Each of those gatekeepers now faces structural constraints, whether from geopolitical realignment, regulatory capital limits, or duration risk. The digital dollar is explicitly designed to route around them.

The GENIUS Act does not describe itself as a sovereign debt management tool. It describes itself as consumer protection legislation. That framing is not dishonest. But it is incomplete. The statute’s reserve requirements, taken in combination with the global-scale ambition of stablecoin adoption, create a direct and automated pipeline from global retail demand to the U.S. Treasury balance sheet. The policy goal and the financial engineering are the same mechanism, expressed in different vocabularies for different audiences.

The strategic logic extends further than domestic debt management. By penetrating the 1.4 billion adults who remain outside the traditional banking system, the United States is not simply expanding the addressable market for its currency. It is reconstructing the global monetary order from the demand side. Every individual who chooses a digital dollar over a local currency instrument is, in functional terms, exiting their domestic monetary system and entering the U.S. one.

That exit does not require a formal policy agreement between governments. It requires only a mobile phone and a perceived need for monetary stability that the local system cannot provide.

The foreign regulatory resistance this generates is telling. When a government bans or restricts dollar-denominated stablecoins within its borders, it is not making a neutral regulatory determination. It is acknowledging that the competitive appeal of the dollar, delivered frictionlessly via digital rails, is sufficient to displace its own monetary authority in the eyes of its own citizens. That acknowledgment, expressed as restriction, is itself the evidence that the strategy is working.

The deeper structural implication is this: the United States is in the process of transforming sovereign debt from a product that must be sold to institutional buyers through auction markets into a product that is continuously and automatically purchased by a global user base carrying dollars in their pockets. The opacity of that transformation is part of what makes it durable. It does not require emergency authorization. It does not trigger public debate about monetization. It presents as an upgrade to financial inclusion and payment infrastructure.

What remains to be seen is not whether this mechanism functions. The legislative architecture and the reserve requirements confirm that the plumbing is being built. What remains to be seen is whether the scale of stablecoin adoption can grow fast enough and into sufficiently large new markets to provide meaningful structural relief on the demand side of the sovereign balance sheet before the traditional buyer cohorts erode further.

If it succeeds at scale, the $39 trillion debt will not disappear. But the question of who funds it will have changed more quietly and more profoundly than the headlines will have captured. A billion new lenders, carrying the dollar in their pockets, will have been added to the U.S. creditor base without a single auction, a single foreign policy negotiation, or a single congressional appropriation to make it happen.

So the Tier 5 conclusion is this: the digital dollar is not primarily a payments innovation. It is a sovereign financing strategy expressed in the language of financial technology. And the most structurally important feature of that strategy is that it does not need to announce itself as one.

References

-

U.S. Congress. Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act). Public Law 119-27, July 18, 2025. Congress.gov

-

The White House. Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law. July 18, 2025. whitehouse.gov

-

Latham & Watkins LLP. The GENIUS Act of 2025: Stablecoin Legislation Adopted in the US. Client Alert, July 24, 2025. lw.com

-

World Bank. Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Washington, D.C., 2022. worldbank.org

-

World Bank Global Findex. Overview: The Global Findex 2025. globalfindex.worldbank.org

-

World Bank Live. Global Findex Report Launch Event, June 29, 2022. live.worldbank.org

-

Congressional Budget Office. The Budget and Economic Outlook: 2024 to 2034. Washington, D.C., February 2024.

-

U.S. Department of the Treasury. Treasury International Capital (TIC) System Data. treasury.gov

Tags

Digital Dollar, Stablecoins, US Sovereign Debt, GENIUS Act, CLARITY Act, Treasury Securities, Monetary Policy, De-Dollarization, Financial Statecraft, Dollar Dominance, Stablecoin Regulation, Reserve Currency, Unbanked Population, Global Findex, World Bank, USDC, USDT, Sovereign Debt Crisis, Federal Deficit, Interest Payments, Currency Substitution, Emerging Markets, Central Bank Policy, Treasury Auctions, Financial Plumbing, Dollarization, Monetary Sovereignty, Payment Infrastructure, Crypto Regulation, Fiscal Policy, National Debt, Digital Finance, Global Monetary Order, Financial Inclusion, Mobile Banking, Stablecoin Market Cap, Treasury International Capital, Congressional Budget Office, Strategic Finance, Geopolitical Finance